Stamp duty was first introduced in England in 1694 and originally covered all paper transactions such as gold/silver purchases, insurance policies, advertisements, newspapers and lottery tickets. Each of these documents required a physical stamp, hence the name. Stamp duty today has dramatically reduced in scope and is levied on security and property purchases, with other areas largely abolished.

The ‘Stamp duty land tax’ refers to the tax levied on property purchases in the UK, which varies based on the value of the property purchase. This was introduced in its current form from 3 December 2014. However, stamp duty has been levied on property transactions for many years. In this article, we will compare the level of stamp duty charged on property transactions between 1984 and 2019, using property purchase prices adjusted for inflation.

Historical stamp duty analysis for purchases of main residential property

The charts below show the output of this analysis prepared using the following methodology:

The stamp duty %’s applied for each year are those applicable at the end of each respective calendar year.

The calculation is based solely on standard property purchases for main residential property, ignoring special rates for first time buyers or second home purchases.

Stamp duty comparisons have been drawn on purchases of £100,000, £200,000, £300,000, £500,000, £1.0 million and £2.0 million.

RPI has been applied to take inflation into account (sourced from the ONS).

For example, a £100,000 purchase price is the equivalent of a £30,108 purchase in 1984 (dividing by cumulative inflation multiplier of 3.32). This would have attracted stamp duty of £301 (based on 1.0%), which is the equivalent of £1,000 today (multiplying by the cumulative inflation multiplier of 3.32).

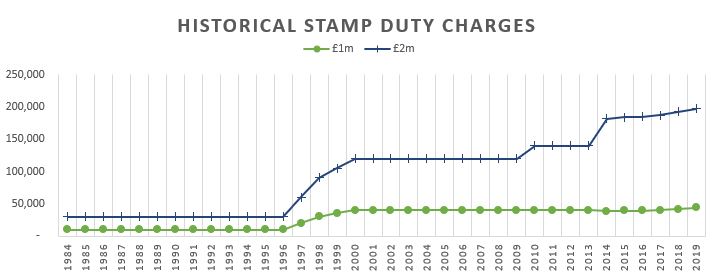

The first chart shows the comparative stamp duty charges based on property purchases of £1.0 or £2.0 million (with the purchase values being reduced historically to provide a comparative analysis, taking account the reduction in the value of money due to inflation).

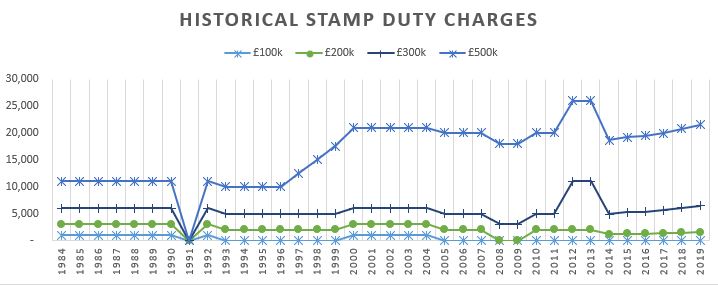

The second chart shows the comparative stamp duty of smaller property purchases of £100,000, £200,000, £300,000 and £500,000 (with the purchase values being reduced historically to provide a comparative analysis, taking account the reduction in the value of money due to inflation).

This analysis shows that from 1996 onwards, the Government has consistently sought to increase the relative stamp duty on large property purchases, particularly in the case of properties transacting for £2.0 million and above.

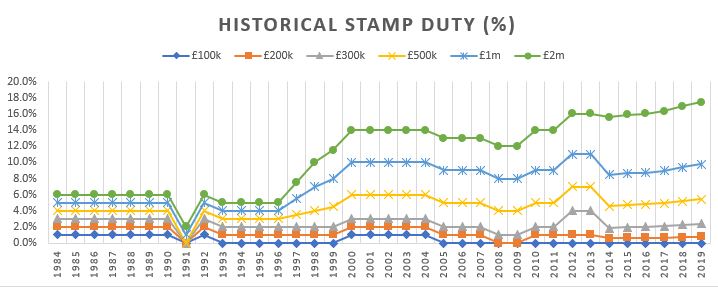

Finally, the third chart shows all property purchase categories on one chart, with the the historical stamp duty shown as a % of the property purchase price.

This analysis shows that purchases of £500,000 were similarly caught by the increases between 1996 and 2000, whilst the relative stamp duty payable on smaller purchases of between £100,000 and £300,000 remaining broadly in line.

Stamp Duty Land Tax Receipts

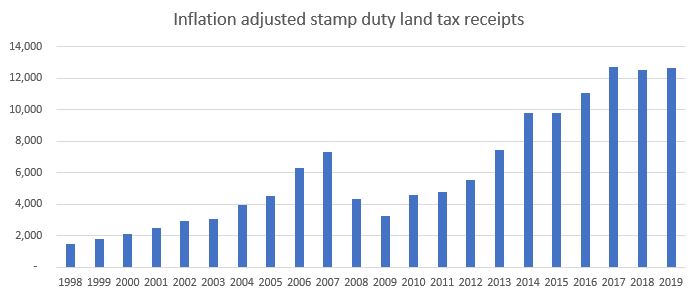

Unsurprisingly, the Government has dramatically increased its stamp duty collections as a result of (i) these rate increases over the years and (ii) house prices rising at levels higher than inflation. The chart below shows stamp duty land tax receipts between 1998 and 2019 (source: ONS) adjusted for inflation. This data shows a 10.7% compound annual growth rate.

Historical stamp duty rates

All rates became effective from the date shown. Note that up until 3 December 2014, the stamp duty land tax was calculated as a singular % of the total property purchase price. From 3 December 2014 onwards, a new banding system was introduced whereby different rates are payable for different portions of the purchase – see the ‘3 December 2014’ section below for a worked example.

The rules were overhauled in December 2014. Prior to this date, the applicable stamp duty percentage was applied to the entire purchase price. Under the new rules, stamp duty rates are only applied to the portion of the property purchase value. For instance, a property purchase of £300,000 would result in stamp duty of £5,000 calculated as: £0 on the first £125,000, £2,500 on the next £125,000 (2% * £125,000) and £2,500 on the next £50,000 (5% * £50,000).

Helen Barklam is Editor of Investment Guide.

Helen is a journalist and writer with more than 25 years experience. Helen has worked in a wide range of different sectors, including health and wellness, sport, digital marketing, home design and finance.

Helen aims to ensure our community have a wealth of quality content to read and enjoy.

")